The Rand has continued it’s run, and continues to confound economists with every turn as it pushes stronger and stronger against the Dollar.

It was an interesting week to say the least, as we saw the Dollar Index strengthen, but the Rand gain ground against the Dollar regardless…

..for once, it would seem to be Rand strength is the reason for the gains, not Dollar weakness.

It was a week of tension too, as the Ukraine situation escalated day by day…and global stocks took a beating.

All these factors play into the emotions in the market, but largely it is smoke and mirrors. Let’s take a deeper dive to see what we can make of it all…

Key Moments (17-21 January 2022)

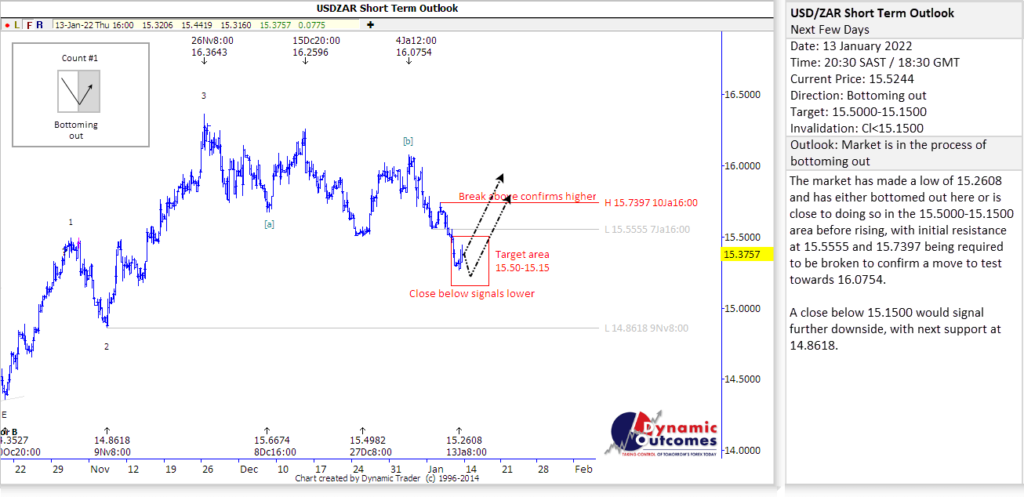

Before we go into the detail of the week, we issued an update on Thursday preceding the week beginning, giving our clients the outlook for the days ahead. The market was at R15.52 to the Dollar and the expectation was that there could be some more downside before we would see the bottoming out, and that we would see a fall further into the R15.50-15.15 area.

Interesting days ahead, that was for sure…

And the week was packed with big headlines:

- Ukraine Crisis – continued escalation in the Russia-Ukraine situation has brought tensions to boiling point, and then at the end of the week, we had Biden ‘predicting’ a Russian invasion…

- Eskom Hike – a huge 20.5% hike is proposed for April for Eskom tariffs, and it has got businesses and consumers up in arms at the huge increase

- SA Inflation – and with that news comes reports that SA’s Consumer Price Inflation hitting 5.9% in December, the highest rate since March 2017…

- State of Disaster – local flooding has caused widespread danger and destruction across the country, to the point that a State of Disaster has now been declared!

- Stock Markets – while the Dollar managed to hold stronger, stock markets did not do as well, enduring massive losses…

Friday brought choppy waters for the Rand, but more gains as we saw the local unit break down to touch R15.25.

And so the week began with the ZAR at R15.33, and all eyes watching closely to see the next moves of the local unit.

And the first half of the week saw losses aplenty, as we saw levels of R15.50 breached once again, with the Rand losing a little ground each day against the Dollar.

It was an interesting turn of events as the Dollar Index made more gains, reversing a lot of losses from earlier this month…

…and this especially interesting in the midst of the Ukraine situation playing out.

It was yet another test for Biden and his administration as to how they would react, as Russia’s intentions became increasingly clear, positioning military assets and around 100,000 troops on the border of Ukraine. Putin clearly has a plan, and he does not like his plans interfered with.

Biden seemed reluctant to commit to anything other than economic response on Russia should they invade, and then also said that if it were only a ‘minor incursion’, it would be get a weaker response from the USA and allies. This brought uproar both locally and abroad – what is a minor incursion and what is a major one?! An invasion is an invasion!

One thing is clear, and that is that Russia is licking it’s lips at the prospect of another 3 years of Biden’s administration – as his lack of decisiveness in drawing a line and being willing to act on it (as Trump did) means that the USA has never been weaker in it’s position of policing rogue nations.

Biden tried to walk back comments on Friday, but it was too late, and you would have to say that the damage was already done. However, as for the Rand, in the midst of all this uncertainty, the tables turned again on the Dollar on Wednesday, and we saw the local unit push stronger against the greenback for the rest of the week:

We also had issued our next forecast on Wednesday, expectant of the Rand breaking yet lower down to the lower target area band of 15.05…

There was such an abundance of action, it was tough to keep up with it all!

To just touch on a few of the other local and global points of interest:

- Locally, Eskom is in the headlines again and this time with another massive rate hike. They are saying that they have no choice, and that this is completely “out of their control”, but there is absolute uproar over the proposal of a 20.5% hike in power costs come April. To make matters worse, it would appear to have gone beyond just a proposal, and seems to be pretty much set in stone, leaving South Africans with no choice.

They say the reasoning for this is two-fold: the requirement to increase purchases of energy from independent power producers and the increase in carbon taxes. Together, these two factors accounted for 13.8% of the proposed price increase, while increases in operating expenditure accounted for only 7.5% and cost escalations in primary energy for 6.5%. - Coupled with that, there was more bad news for consumers as SA’s inflation hit 5.9%, the highest level since March 2017. Some examples are prices of food and non-alcoholic beverages increased by 5.5% in the year to December, while transport prices jumped by a whopping 16.8%, fuelled by rising petrol and diesel prices. This in combination with the electricity increase coming in April makes for a rather cloudy future of consumer morale…

- And not to go on about the bad news, but there was also the State of Disaster that SA was forced to declare following the incredible flooding we have seen over the last few weeks. For a country that battles so much with drought, it is ironic that things can turn so fast with the abundance of water that is beyond what dams and rivers can handle! Enormous damage has been caused, prompting the State of Disaster declaration…estimated needed funding to fix all the damage in KwaZulu-Natal is already R3.3bn!

- Getting back to global markets, with the tension over Ukraine and other global factors, US stock markets tumbled, with the S&P500 and Nasdaq heading for their worst week since the crash of February 2020. In the final hour of trading, stocks continued to extend their losses, with the S&P500 down 6% and the Nasdaq down 7.5%.

This week has seen long term trendlines being broken and strong levels of support being brushed aside. Has the boom-time party finally come to an end? Bitcoin also suffered large losses as uncertainty gripped every market…!

But then getting back to the local unit, we saw the Rand push stronger yet , touching R15.06 on Friday, the strongest levels we have seen since November last year when things really began to unravel. What a week it had been! This next week of activity is going to be nothing short of fascinating…!

The Week Ahead (24-28 January 2022)

So looking to this week ahead, we are watching closely to see what happens with two of the biggest events of 2022 so far: SA & the US’s Interest Rate Decisions.

One feels these will help set the tone for what sort of a year we are in for as the Reserve Bank analyzes the situation the other side of the holiday season and shutdown.

For the US, inflation is soaring and there is a lot to consider for the Fed.

And then outside of economics, but influencing everything, we have the Ukraine & Russia situation. This will be capturing headlines until things go decidedly one way or the other…

In terms of a full list of events we are looking at, these is what we’re watching:

- SA – Interest Rate Decision

- US – Goods Trade Balance, Interest Rate Decision, Jobless Claims, Durable Goods Orders, GDP Growth Rate

Once again, we will be shutting out all the noise and focusing on what the chart wave structures and cycles are telling us – and watching some key levels to confirm our most probable outlook for the days and weeks going into yearend. Until next week!

If you have any questions or feedback, please let me know.

To your success~ James Paynter