Never underestimate the Rand is an old saying we have had to come back to over the years, time and time again… just when everyone is writing the ZAR off, that is the moment you know that sentiment is about to turn.

Has it been anything different this year?

No, once again, it has been a case of these wild swings of fortune (read sentiment).

And what we have seen this last week has been the market once again breaking stronger versus the Dollar… testing levels last seen in March before even lockdown was announced.

It is no small feat to be 320c and more than 16% in the green since April’s disaster zone. Who would have thought?

Let’s get into the full review and show you how you could have seen this coming.

Key Moments (7-11 Sep 2020)

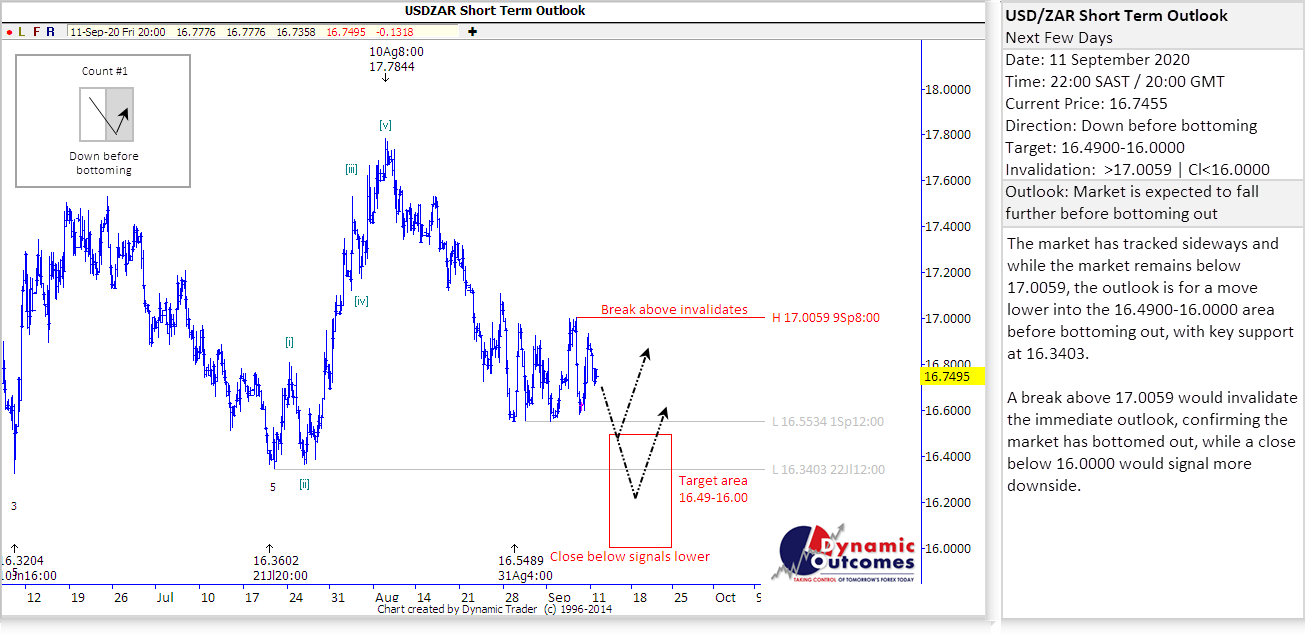

So, before the week began, we issued our forecast on Friday with the USDZAR trading at 16.74, having endured a very up and down week of testing R17/$.

Our forecast showed the outlook for the next few days: the ZAR was expected to strengthen, breaking down toward a minimum of 16.49, with the bottom of the target area being 16.00, before we could expect to see a retracement…

It was, once again, going to be an interesting few days if this was to be believed…

And interesting it was, with some big headlines along the way:

- SARB nationalization – the much feared nationalization of the Reserve Bank received a massive update this last week…

- Level one – lockdown will finally take another step towards normal, with September 1 bringing big changes for SA thanks to Ramaphosa’s announcement

- Stimulus – both SA and the US seemed to move inch forward with economic & stimulus plans, much to the delight of all.

So, Step 1 – markets opened on Monday with the Rand trading a shade over R16.70…

It was going to be a big week, with a host of global events playing out, providing plenty of triggers for the Rand – which also meant plenty of risks.

But really, when it came the ZAR, the biggest event of the 5 days was the ANC’s announcement on SARB’s nationalization.

Now, we will all remember that while this has been a topic of debate for years, this became a pertinent issue again after the 2017 ANC conference, with it being labelled as high on the agenda for the ruling party… And has since been playing out in stages since then.

Well, as expected, this pandemic and economic crisis has made some major changes to the ANC’s plans.

Whether this is entirely related to the economic situation as they claim, or more to do with terms of IMF and other bank loans, we may never know… but this last week, the ANC announced a hold on all their plans to nationalize the Reserve Bank.

The reasons noted were that resources needed to be channelled elsewhere – and effectively that there are bigger fires to fight.

This will not please the EFF, but is a welcome respite for concerned locals and investors alike – but it is worth noting that this is only a stalling of their Communist agenda, not a completely abolition…and this will come up again, perhaps even in the near future.

And, while this was going on, the Rand took full advantage and took strides stronger against the Dollar:

Just as per our forecast, we broke well into our target area, until we were testing R16.15 on Thursday evening.

And that wasn’t the only big piece of news, as Ramaphosa’s economic recovery plan got the green light from business, labour, community, as well as representatives of government…

The difference between a failed state and a massive recovery is ever so slight, and this plan will be at the heart of what happens.

And then in other news…

- The other major local news for the week was Ramaphosa’s announcement on Level 1 Lockdown – it looks as if life could be taking one more step toward ‘normality’ again, with the cabinet deciding on Level 1 restrictions from midnight on Sunday, 20 September. So today marks the first day, and SA will be hoping this combined with international travel from October 1st will begin the kick-starting of the economy.

- Brexit is at the forefront of the headlines again after Boris Johnson had his divorce deal pass its first hurdle on Monday, despite some disagreement among senior members of his own party. This meant that the Internal Market Bill would be pushed to the next stage in parliament. The bill will rewrite some of the Withdrawal Agreement with a focus on maintaining the UK’s economic and political integrity. Boris Johnson is beginning to take some heat over this, as negotiations drag on without any clear way forward.

- The Federal Reserve’s interest rate decision along with its press conference and economic projections was due to shed some light on how the US economy is coping – and what the Central Bank’s plans are moving forward. And they made a clear statement that there are going to be no rate hikes for years, perhaps until 2023 – which is also when they first expect their inflation to hit the 2% target. SARB also kept rates on hold at 3.5%, despite the fact that the growth outlook is now at -8.2% for 2020.

- Also in the US, Trump indicated that lawmakers must go for a bigger stimulus proposal as all this money comes back to the US in the end anyway. This will potentially bring some form of a compromise between Democrats and Republicans to get a bill passed into law to release the much needed funding. This will be a big one to watch going into next week.

As for the Rand, it enjoyed some of the best levels in 6 months, with a break to as strong as 16.08/$ on Friday!

What a week it had been, as telegraphed by our forecast, 7 days before… as the Rand closed out around R16.25/$ at the South African end of day!

The Week Ahead (21-25 Sept 2020)

As we look to the week ahead, there is very little happening locally with Heritage day on Thursday the 24th, but internationally there are a number of smaller events:

- USA – Multiple Fed Powell speeches, Treasury Sec Mnuchin speech, Durable Goods Orders, Jobless Claims

- UK & EU – Inflation Reports, BoE speeches

So plenty to digest and occupy the market this coming week, as we await further news on Stimulus in the US and economic recovery plans locally. And, of course, another week closer to US elections with things really starting to hot up.

And once again, while the economists of this world will look for market direction based on these events, data and news… we will instead be focusing on what matters – what the market itself is telling us and where evolving patterns of sentiment are likely to take us based on our Elliott Wave based forecasting system…

…which served us and our clients very nicely last week!

And based on what it is telling us now, it is likely to be another fascinating week…

If you have any questions or feedback, please let me know.

To your success~

James Paynter