The perfect storm has hit, and the Rand had a rough ride initially as a result… only to pull it back towards the end of the week.

That was the long and the short of it from this last week, as the combination of global and local events took hold of the headlines, to keep stirring the frantic markets.

With less than 24 hours until the polls open for the grand finale (or not) of the US election, there is so much more coming soon.

But first, let’s take a look at what transpired in the last 5 days, to give us some insight into the crazy weeks ahead.

Key Moments (26-30 October 2020)

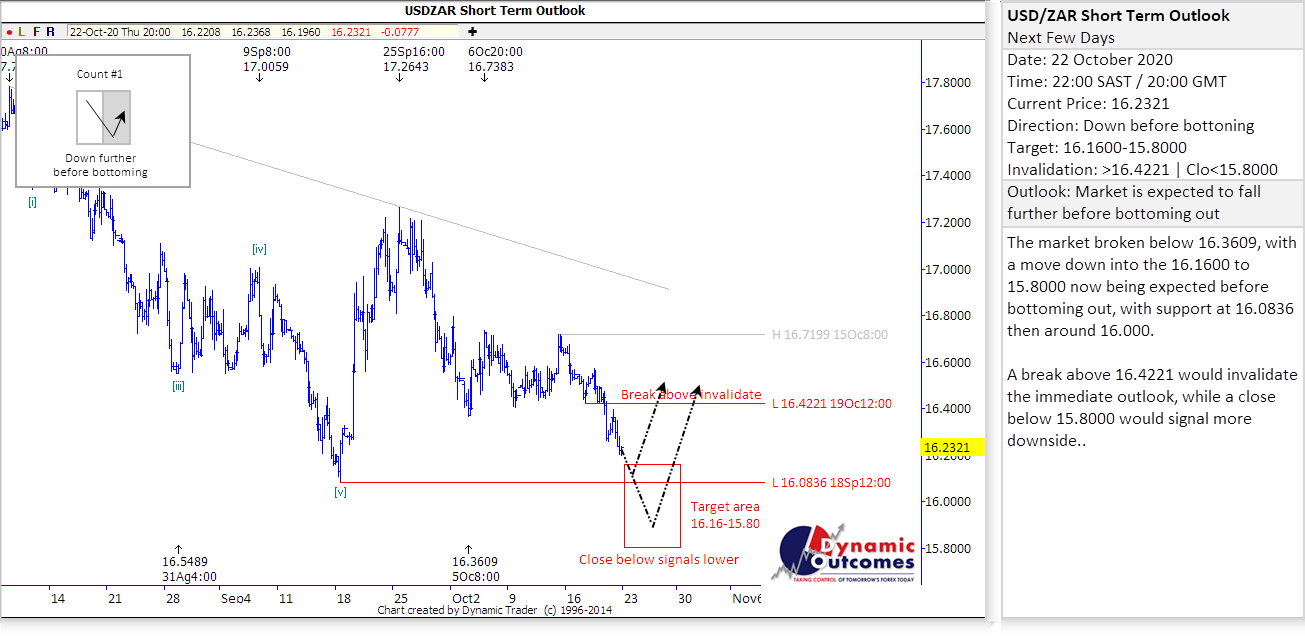

Before the week began, we issued a crucial update to our clients on Thursday the 22nd of October to all of our paying subscribers, warning them of what the days ahead held.

The Rand was at R16.23, and we were seeing a break lower coming into the target area of R16.16-15.80, before we would then see the market bottom out.

And then it was just to wait for the triggers… and come they did:

- Mid-Term Budget – with so much expectation for Mboweni to fix every problem with the click of his fingers, chances were that the speech was going to be a disappointment…

- US Elections – with more than 50% of the 2016 election’s total votes already cast, the election is almost half over! But when will it finish…?

- Europe’s Wave II – the next massive wave of the pandemic is sweeping across the EU, and fears are now of a second lockdown…

- US GDP – an explosive return in Q3 came right on cue for Trump, as economic figures indicated a big bounce back after Q2’s lockdowns

So, take a breath…let’s start with local news first.

With the Rand opening trade around R16.30 on Monday morning, we were watching to see the move stronger over the coming days into our target area.

And as expected, the Rand strengthened down to as strong as R16.08/$ on Tuesday as per our forecast from the previous week… so now that left the Rand primed to bounce upwards from these levels.

What it needed was a trigger…

Which left us awaiting Wednesday’s Mid-Term Budget Speech – with high expectations for Mboweni to right the wrongs… but it didn’t go quite according to plan.

He painted a dour picture, with a speech filled with worry, giving many a difficult time looking for the positives:

- Reductions to the public wage bill will narrow the budget deficit and stabilise debt over the next 5 years

- Social compact agreed to prioritise short term measures to support the economy, involving government, business, labour and civil society

- The Medium-Term Budget Policy Statement aims to cut non-interest spending by R300 billion

- R10.5 billion will be allocated to SAA to implement its rescue plan

- Treasury expects the economy to shrink by 7.8% in 2020, rebounding to growth of 3.3% in 2021

- SA is spending 21 cents of every rand just to pay existing debt, and this will get worse

- SA is only expected to rebound to pre-pandemic GDP in 2024

- Tax revenue will decline by R312 billion in 2020

- SA’s debt now sits at a staggering 81.8% of GDP, up from 63.3%

While risks abound, there are some particular ones which are clear worries to recovery plans:

- Weaker than expected growth, with many moving variables this is a serious threat to any plans for growth in SA, which is much lower than growth expectations for emerging markets

- Continued deterioration of public finances, tackling corruption and ensuring frivolous spending is eliminated

- Second-wave of the pandemic, economic restrictions (lockdown), would drastically impact outlook

- Failure to implement structural reform, shift spending to investment (capital goods to grow at 7% per year).

Final conclusions were that Mboweni is once again making the best of a bad situation, apart from yet another nonsensical SAA bailout (likely not his doing but from higher quarters)…but will it be enough?

The ‘simple’ answer is: Commitment and Implementation!

But can this be done?

Well, that is the question going forward – and the Rand didn’t take a liking to that pathway ahead, bouncing up to hit R16.49/$ by Wednesday afternoon.

Another move called perfectly by our Elliott Wave based forecasting system, as the market bottomed out in our target area!

And then in other news over the pond:

- Europe is in Phase 2, as Germany and France prepare to announce a month-long lockdown, as deaths across the region jumped almost 40% in a week – signalling that an economic recovery is nowhere in sight. Angela Merkel warned of a “long, hard winter”, as everyone braced for the worst in the Northern Hemisphere. Boris Johnson is now under pressure to do similar in England, and likely the pressure will increase on nations surrounding. Phase 2 of the epidemic is inevitable – but do lockdowns really help is the question? To make matters worse, there are now warnings too of another variant that is spreading across Europe…

- Also in the UK, they and EU seem to be coming to terms over a ‘Brexit’ deal as French President Emmanuel Macron stated he is open to negotiations with regards to an agreement over fisheries. This will hopefully see the divorce finalised by mid-November according to negotiators.

- Back in the US, with election day now just a few hours away, this is without a doubt the most unique election in history. With more than 50% of the votes already cast (based on 2016 turnout), the election is in essence half over already – yet it hasn’t begun…! The real question though is this: when will it end? The change to so much mail-in voting has a couple of key problems – firstly, is there the capacity in USPS to handle this influx, and will it be done without any votes being spoilt? Secondly, how long is this stream of voting and counting going to take, because by current reports, we are not going to be seeing a winner on the night of 3rd November? Lastly, recounts or court actions as a result of election disputes are VERY likely considering the amount of uncertainty around this election. And so we go…

- Right on cue for Trump’s economic claims, the US GDP for Q3 came in at a whopping 33.1%, better than the expected 32%. A surge in business and residential investment along with stronger consumer activity helped the economy after its worst-ever quarter in Q2.

And just like that, we were on to Friday… and out of the blue, the Rand turned the tables once again, trading down to test R16.20/$ again.

It was a real topsy-turvy week, and don’t expect it to stop as we head into the US election finale!

The Week Ahead (2-6 November 2020)

This week ahead is all about the global focus – and in particular in the US, with some gamechangers coming over the next few days…

- USA – Presidential Election, Trade Balance, Jobless Claims, Fed Monetary Statement, Interest Rate Decision, Non-Farm Payrolls

- UK & EU – BoE Interest Rate, Monetary Policy & Minutes

Don’t expect these to be the only talking points, but as we look to the days ahead, you can hardly look further than the US election. While it may seem far away happening the other side of the pond, this result will have a profound and measurable result on the global economy in the years to come – no country is exempt.

The election promises to be closer than many are expecting – as always, polls are narrowing in the closing days (if any of them can be believed, based on the abysmal accuracy in the 2016 election).

As for the Rand, expect plenty volatility once again. We will keep looking at our Elliott Wave based forecasting system to give us some clues, with some key levels that we will be watching to confirm the larger degree trends.

Another interesting week lies ahead!

Simply use the link below to get access now. No charge. No card. All yours to trial for 14 days. Click here to access to our forecast from Friday on the house!

If you have any questions or feedback, please let me know.

To your success~ James Paynter