Eskom trouble for some time, but this week things have really taken a turn for the worse, sending the power utility into crisis mode.

From being close to keeping up with demand to moving to Stage 4 load shedding was nothing short of a disaster, and it really gave the ZAR the jitters.

How had things gotten so bad, so quickly?

With Eskom, unfortunately you are always one step away from disaster. However, it has prompted some massive changes in the electricity space – so let’s get into the full review, to see how this is going to affect business, the economy, and ultimately: the Rand.

Key Moments (7-11 June 2021)

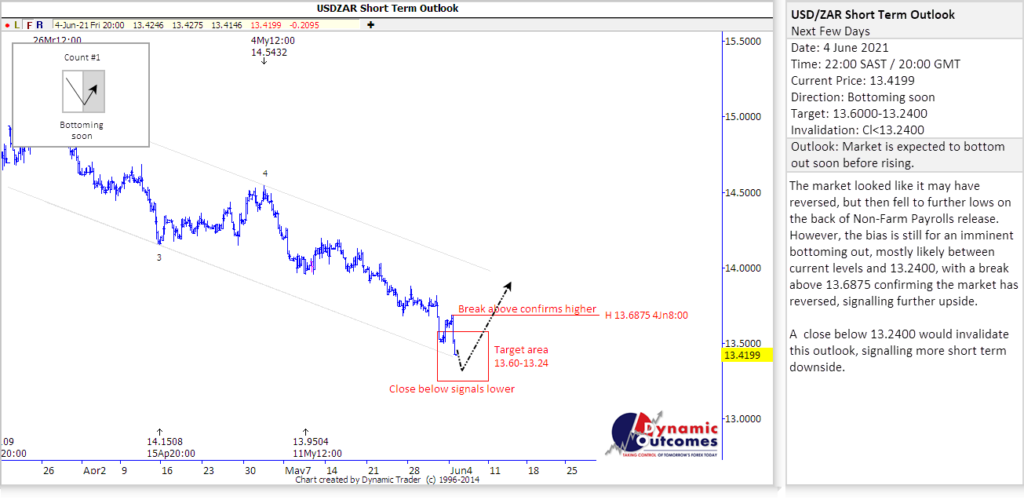

Before we get into the week, this was our outlook for the USD vs ZAR on Friday the 4th of June. With the ZAR trading at R13.41 to the Dollar, the expected trend was for it to bottom out above R13.24, and the move higher to test above R13.6875…

So now it was just to look for the triggers, along with the Eskom worries.

Here were the other big headlines from the week:

- US-China Tensions – the two juggernauts continue to battle back and forth, between the origin of the pandemic, trade talks and now the investment blacklist issued by Biden…

- GDP Figures – local figures which give an idea of how effective economic recoveries have been were coming thick and fast, and this week it was SA’s GDP

- CPI & Inflation – also big indicators of the potential inflation crisis were aplenty, even as the Fed indicated that their belief was that it was temporary

Now firstly, let’s start with the opening of the Rand…

Trading around R13.40, the local unit had now broken into the lower R13s, and was really starting to have economists and businesses alike in absolute disbelief due to the amazing run of strength.

However, when these extremes are hit, you know a market is due to turn.

This week, it appears Eskom provided that catalyst for the move.

As the week progressed, so did the levels of load shedding, steadily moving up through stage 2, stage 3 and eventually stage 4 by Wednesday.

This was a crisis, make no mistake about it! You can talk about an ecomomic recovery “until the cows come home”, but if you have no electricity, the economy is dead in the water.

CEO André de Ruyter’s take was that “there is clearly a gap between the assumptions of what Eskom should do and the reality of what it is able to deliver” and that “Eskom’s energy availability factor is far below the assumptions made in the Integrated Resources Plan of 2019”…

To be fair, he is stuck between a rock and a hard place – the power utility is hopelessly outdated, under-maintained, and now needing to comply with new environmental legislation. So he cannot work miracles, but all the while, the country is losing money as a result of the utility’s failures.

But, there are some positives to draw from this – and they came in the way of real change in the electricity space for SA:

- Ramaphosa made a major decision to allow businesses to be able to generate up to 100 megawatts each!

- The previous level had been 1 megawatt, with talk of it being moved to 10, even although the business sector wanted a minimum of 50MW.

- With the President twisting Energy Minister Gwede Mantashe’s arm, this new 100MW limit will be put in place

- For comparison, 100 MW could power two large mines in South Africa. One of Koeberg’s two units produce 900 MW – so just nine companies could together produce a similar load.

This was huge news, and has the potential to create massive change in the electricity supply, as well as producing extra jobs and investment into the country…so maybe the final straw snapping was good news in the end! But the Rand did take a hit as a result, moving from it’s pretty position to upwards of R13.75!

And then in other news:

- Then looking abrooad, traders and investors alike were also keeping tabs on any updates on US-China relations following President Joe Biden’s release of an investment blacklist, where he almost doubled the number of Chinese firms that Americans are banned from investing in. This comes just as trade talks are restarting for the first time since Biden took over, and the next few months are going to be especially interesting to see if the hard line of the Trump administration will continue, or if Chinese pressure will prevail…

- The RSA growth numbers came out during the course of the week, showing a real growth rate of around 1%. While not a huge figure, it does provide hope, showing that the country is making use of what is available to get things done. However, gains like these are extremely small in comparison to the previous losses – and SA has not seen the V-shaped recovery that other countries have. There are other big prospects though, such as the new citrus export deal with the Philippines, which will contribute to the expected 500k ton growth of the industry in the next 3 years. These negotiations with the Philippines have lasted 12 years, and finally there will be some ‘fruit’ from them!

- Then over in the US again, we had more interesting developments on the inflation debate, as CPI rose 5% year over year in May, the fastest rise since August 2008 which was the midst of the previous financial crisis. Yet still, the Fed seems reluctant to act, and Economists said there are signs that rising prices could be temporary since they are centered in areas impacted by the pandemic. We will wait and watch this one closely…

And getting back to the Rand, the market played a bit of yo-yo through Thursday and Friday, but eventually swung back again to end around that R13.75 mark again.

Despite the volatility, the Rand had played out the week as we had expected with our forecast, moving from the lower target area to test higher levels the Elliott Wave based forecasting system had called it again.

The Week Ahead (14-18 June 2021)

As we roll onwards towards the halfway mark for the year, there are few events of note to watch in the coming week:

- SA – Retail Sales

- US – Retail Sales, Interest Rate Decision, FOMC Projections, Fed Monetary Policy, FOMC Press Conference

- EU & UK – Consumer Price Index

The big possible mover would be out of the Fed, but plenty else to keep the market on their toes. As for the Rand, the next week could prove pivotal, with some key levels being watched to confirm whether the Rand’s fortunes have finally reversed, or whether the local unit has any further gas in the tank.

Please take our Rand forecasting service for a test-drive! This will give you access to the same charts we are to give us and our clients the likely direction of the Rand – ahead of time, enabling you to make educated and informed decision. Simply use the link below to get access now. No charge. No card. All yours to trial for 14 days.

Click here to access to our forecast from Friday on the house!

If you have any questions or feedback, please let me know.

To your success~ James Paynter