Well, now it is official… The Rand party is over. For some (namely, exporters), it couldn’t have a come a moment too soon.

With the incredible run of all of 597c from 6 April 2020 through to 6 June 2021, when the market finally bottomed having come from R19.33 down to R13.36, the Rand has rightly made headlines.

This is an amazing performance for an emerging market under pressure in the midst of a pandemic… and clearly counter to any rational logic.

So when we had reached that level a couple of weeks back, most persons had reached that extreme level of emotion. For exporters, it was fear and panic. For importers, it was greed and complacency.

This is a red flag. And our Elliott Wave based forecasting system confirmed it.

And just like that, we were back over R14/$. Did you see this move coming? Read on to see how you could have…

Key Moments (14-18 June 2021)

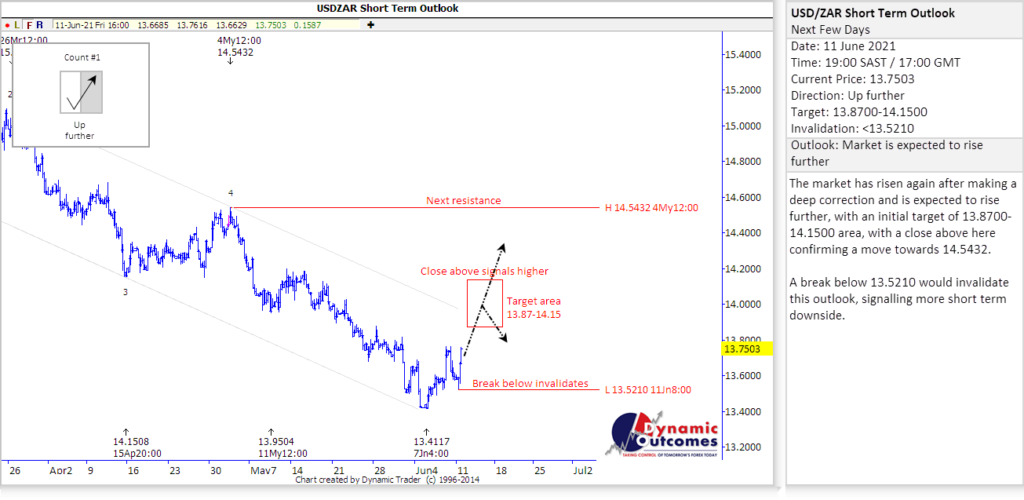

Before the week began, we issued our forecast update to our subscribers. Our 11 June 2021 Short Term Forecast showed the market at 13.75, with a target of R13.87-14.15 in the coming days.

The prediction was clear…now to watch for the action, as we watched the Elliott Wave count playing out.

And these were the big headlines for the 5 days that we looked for triggers from:

- Fed Panic – all of a sudden, the tables turned, and the Fed’s denial of inflationary issues was no longer…what happens next?

- Level 3 Again – in another about-turn, Ramaphosa sent SA back into the doldrums with new level 3 restrictions…

- G7 Conference – the high profile event of global leaders was the focus of attention as all eyes were on the Biden-Putin relationship

- Jobless Claims – the US continues to be shaky in job recovery with inconsistent months of jobs added, giving mixed indications of the global economy’s strength

And so the week began with the Rand trading at R13.71, and largely Monday’s trade was very quiet. But on Tuesday, the triggers started to come.

Ramaphosa announced the long anticipated (or rather, dreaded) return to lockdown level 3.

This will affect businesses and gatherings with curfews, and just generally add more levels of complexity to daily life – a surefire way to stumble the economy all the more.

This is not what is needed now, just as SA was looking to round out the second quarter with some good growth … how much longer will countries go through these endless cycles of authoritarian lockdown-open-lockdown, despite there being no evidence that they have done any good whatever, in fact, the contrary?

The Rand edged higher on this, moving upwards of R13.80 …but the real trigger was yet to come.

On Wednesday, which was a holiday locally, was the big Fed meeting – and there came the shocker of the week.

A sharp change in direction by the FED regarding their interest rate timeline saw a big pull back by major investors.

Whilst the changes outlined during the meeting don’t seem to be planned for any time before the end of 2023, the switch to a more hawkish stance shows that the FED can in fact be surprised (despite truckloads of info) and nothing is ever set in stone.

From months of saying that they are not concerned about inflation, they suddenly considerably raised their expectations for inflation this year and brought forward the time frame on when it will next raise interest rates.

But still, their massive bond-buying program continues… So it is a strange situation, and things remain murky – and the markets did not like this change…

The Rand ripped weaker, smashing nearly 30c in an hour to head back over R14/$ before the end of the day!

And this was all while SA was not even at work…showing the power and ability of global markets to affect the Rand’s value. Whilst a weaker rand is less than ideal for consumers of import reliant goods, as an export heavy country, this may help the economy to get back on its feet.

And then in other news:

- All eyes were on the G7 during the course of the weekend and then all of the subsequent events after, but none more so than the much anticipated meeting between Biden and Putin. This is now the first of major consequence since Biden’s inauguration, and many were waiting to see if he would stand up to Putin. The meeting went off mostly as planned, and Biden called it “positive” and said he “doesn’t think Putin is looking for a Cold War with the United States”. He also said saying he made “no threats” to his Russian counterpart, but warned of “consequences.” While we probably will never hear what all was said, it would seem Biden was not the hardline attack dog against Putin that was promised.

- He had other worries locally, as jobless claims continued to indicate that the US was not yet out of the woods. Essentially all the increase came from Pennsylvania and California, as claims rose 52,000 above the estimate of 360,000 to hit 412,000. While these are small numbers in comparison to other countries, it is not the trajectory that the US wants to see. They will continue to monitor these and the US recovery closely.

- Global markets were in an absolute whirlwind following the Fed’s meeting which provided the perfect trigger to the underlying sentiment. The Dollar was oversold – the trigger meant that the Dollar Index rushed back over 92 and EURUSD way down to $1.18. Gold was the inverse, with being majorly overbought, and it suffered a big correction down to $1770. It is always fascinating when we get to the tipping point of these cycles and you see the sentiment turn once again… Our Elliott Wave-based forecasting system called these moves on EURUSD, Dollar Index and Gold – if you are interested, please go here for our forecasts on those markets.

Friday saw the Rand testing R14.30/$ levels as it was clear that that the last two weeks had totally changed the momentum in the markets.

This move was right in line with our other outlook that we had issued on Wednesday, indicating that the Rand would push higher toward R14.30.

The waves of emotion are an amazing thing to watch – I just trust you had the guidance you needed to make the right decisions… And that was the wrap!

The Week Ahead (21-25 June 2021)

This next week is setting up to be really interesting, with a bunch of events set to take place, providing more triggers for the market. The market will be on high alert after the volatility following the Fed’s meeting, so expect more nervousness and volatility as markets take stock of where things stand.

Here are some of the noteworthy ones:

- SA – Inflation Rate

- US – Fed Powell Speech, Jobless Claims, Trade Balance, Durable Goods Orders, GDP

- EU & UK – Interest Rate Decision, Monetary Policy Summary, BoE Minutes, GDP, Consumer Price Index

As for the Rand, we have now reversed fortunes, and while the bias is for more Rand weakness, it is unlikely to be all one way traffic, and we will be watching some key levels the next week, based on our analysis. We suggest you do the same!

Please take our Rand forecasting service for a test-drive! This will give you access to the same charts we are to give us and our clients the likely direction of the Rand – ahead of time, enabling you to make educated and informed decision. Simply use the link below to get access now. No charge. No card. All yours to trial for 14 days.

Click here to access to our forecast from Friday on the house!

If you have any questions or feedback, please let me know.

To your success~ James Paynter