Well, well… as the endless repetition of the tightening and easing of mindless, ineffective lockdowns continues, the future remains as uncertain as ever. For once, this past week it was a move in the right direction for SA as the country headed back to Level 3.

For how long, is the question?

The indecisiveness of governments and using draconian methods proven to be completely unsuccessful means nobody quite knows what is going to happen next.

For now, the Rand caught a bit of a break.

But long term signs are worrying due to IMF and other institutions views on the economy. Let’s take it one step at a time, and dive into the full week’s review…

Key Moments (26-30 July 2021)

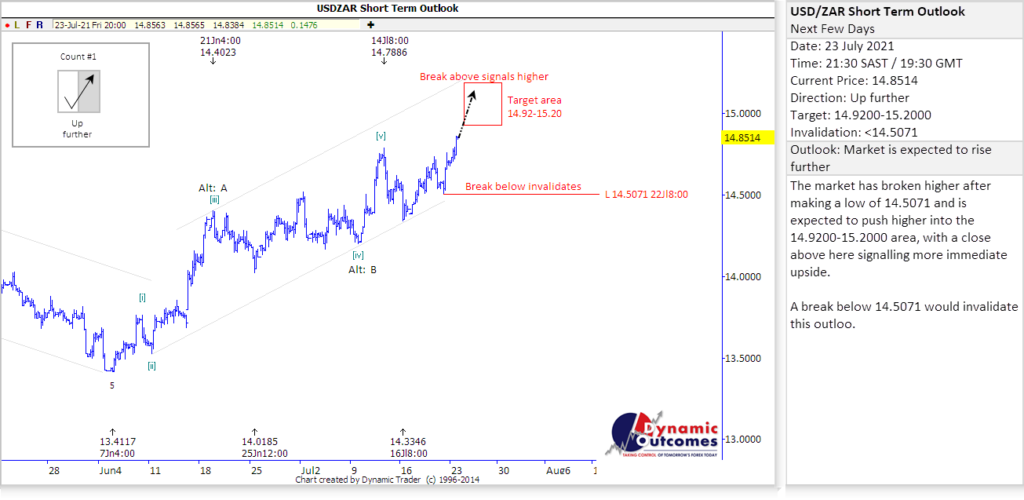

Before we the week began, on Friday we had the market at R14.8514, having endured losses throughout to the Dollar. Our forecast was issued with the outlook for the coming days, giving guidance to our subscribers. The view was clear, with the market expected to push even higher to target toward R15, into the R14.92-15.20 target area.

So, before the week had begun, the call had been made about where we would go…now it was just to see how it worked out.

News often provides triggers for movement, and these were the biggest headlines from the 5 days:

- Level 3 – Ramaphosa’s announcement of one step in the right direction meant that SA was a step closer to normality, but how long would it last, and how much of a difference would it make?

- Tiger Brands – massive losses incurred for the huge company, as they were forced to do a far-reaching recall…

- Fed Updates – investors remain on tenterhooks, awaiting every snippet of info from the Fed about how they see the next year playing out…

- Mango Airlines – another airline, another business rescue…how many more airlines are going to fail?

So, the week began with the best news possible, that SA had downgraded from level 4 to level 3 in terms of lockdown restrictions, thanks to Ramaphosa’s announcement.

What did this mean?

Well, these were the changes to Saffers’s life:

- The evening curfew will remain in place from 22h00 – 04h00;

- Interprovincial travel can resume;

- Non-essential establishments, such as restaurants, gyms and fitness centres, can operate but must close by 21h00;

- The sale of alcohol from retail outlets for off-site consumption will be permitted between 10h00 and 18h00 from Monday to Thursday. Alcohol sales for on-site consumption will be permitted as per licence conditions up to 20h00;

- Gatherings are allowed but are limited to 50 people indoors and 100 outdoors. Only 50 people are allowed to attend funerals;

- Schools will be allowed to reopen as of Monday (26 July).

Small changes, at least something – yet not nearly enough, considering that these measures have proven to have no beneficial effect whatever – in fact, just the opposite!

But surely good news for the Rand after a tough previous week?

You would think so…

…but it was quite the opposite, as we saw the local unit weaken to a touch under R15/$, hitting R14.99!

This brought it right into our target area as promised on Friday, as the market was once again acting the opposite to what logic would suggest. But from then on, the tide of the week turned.

And for consumers and importers, it could not have come a moment too soon, as the worrisome R15/$ level was not one locals wanted to see again – but a level that exporters welcomed, having not seen these rates since 4 months ago.

And then in other news:

- Tiger Brands suffered a tremendous blow this last week as 20 million canned products sent out from their factories had to be recalled. This amounts to 9% of annual production and is estimated to be up to R650m in goods that will be lost, due to concerns over potentially defective cans. Just on Monday, shares of Tiger Brands dropped all of 6.4%. This is the kind of trouble that South African businesses, big or small, just don’t need right now!

- Heading over to the US, through the week the Fed gave different updates and

economic insights which were watched by all. With a two-year debt limit

suspension set to expire at the beginning of August, US Treasury

Secretary, Janet Yellen, urged Congress to raise or extend the debt

ceiling to avoid running out of cash by October/November or risk a US

government default. Republicans refused to vote for a debt ceiling

increase, blaming Democrats for pushing legislation that led to an

increase in inflation. It is Congress’ favourite game of chicken, and it

tends to plays out every few months.

The FED also tried to ease investors’ minds as they stated interest rates would remain as is, for now at least. Chairman Powell also re-iterated that while they were making progress on their end goal of self-sustaining markets, they were still a while off from pulling all support. - Locally, the S&P rating agency issued a statement saying the looting that disrupted the country in recent weeks, could negatively affect 2021 growth by up to 0.7%. The International Money Fund (IMF) also released a report that analyzed the post pandemic recovery of the world’s major economies and the rainbow nation found itself on the wrong end of the list, as they anticipate SA to have the 2nd weakest growth rate in 2022…Eish.

- Another day, another airline into business rescue. Mango Airlines is the latest case of disaster control, following SAA having done the same just a few months. Mango, a subsidiary, has now followed suit – effectively declaring bankruptcy. It remains to be seen how this one plays out, but this is really just a case of another SOE related firm facing the same treatment and needing urgent help.

- On Thursday, we saw US GDP numbers pointed towards a still off-balance economy, with 6.5% growth in Q2, as opposed to 8.4% which was the expected number. While definitely on the right path, the FED stated that they would continue to artificially prop up the US economy for a little while longer.

And eventually getting back to the local unit, we saw the market inching its way back, particularly after the US GDP announcement.

Before we knew it, on Friday we were back testing nearer R14.50 level once again, eventually closing out just over the R14.60 level.

What a week it had been, despite all news, the Rand had managed to turn things around…

…or rather, the Dollar’s weakness had given the Rand some respite once again. Either way, it was a welcome bit of relief for locals! And that was the wrap!

The Week Ahead (2-6 August 2021)

And just like that, we are through July and into August.

This next week does not have a ton of events, but the ones that we do have are known to be some of the larger triggers, with Nonfarm Payrolls being the biggie:

- US – Jobless Claims, Trade Balance, Nonfarm Payrolls

- EU & UK – BoE Interest Rate Decision, Monetary Policy, BoE Minutes

The Rand has had some respite for now, but the question is for how long?

We have some levels we are watching which should give some indications for the days and weeks ahead – once again, we will continue to filter out the noise and simply follow the what the charts themselves are telling us as to how far, based on our Elliott Wave based forecasting system.

Please take our Rand forecasting service for a test-drive! This will give you access to the same charts we are to give us and our clients the likely direction of the Rand – ahead of time, enabling you to make educated and informed decision. Simply use the link below to get access now. No charge. No card. All yours to trial for 14 days.

Click here to access to our forecast from Friday on the house!

If you have any questions or feedback, please let me know.

To your success~ James Paynter