And the Rand rollercoaster continues… Just as the market thought the Rand was trending stronger, everything turned on its head again.

This time it was right from the start of the week, as the USDZAR ‘gapped’ all of 23c from the close on Friday to the opening on Monday.

It was a bad start to the week, and the trend continued!

But there was a lot more to the week than just the opening of trade… …and we are here to take you through it. Read on for the full review!

Key Moments (22-26 March 2021)

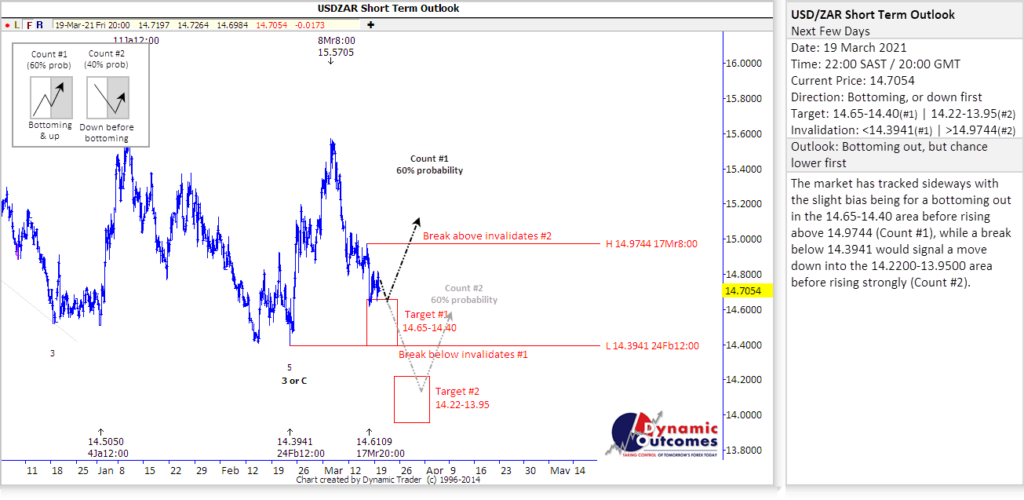

Before the week began, we issued our forecast update out to our subscribers on the USDZAR on Friday the 19th. This was the Short Term Update for the next few days, and it showed that we were most likely nearing a bottom in the market and could expect ZAR weakness soon. We expected that we had either already bottomed, or were about to in the 14.65-14.40 area, with an alternative (less likely) count of heading lower first.

It was always going to be an interesting few days with a forecast like this!

And it was interesting too from a news point of view. Here were the main talking points from the week:

- Interest Rates – the hold continued as SARB continued to monitor the economic hole that SA needed to dig itself out of…

- Suez Snarl – the major shipping route has had an unprecedented blockage, with a massive cargo ship being stuck across the 300ft wide canal, stopping billions of dollars of trade every day.

- Eskom Debt – the ever increasing sum is becoming a massive headache, and is reaching a point where the Treasury must make a decision.

- Oil Retreats – as fuel prices soared globally, finally Oil has finally retreated to it’s cheapest pricing in 6 weeks.

So, back to the Rand…

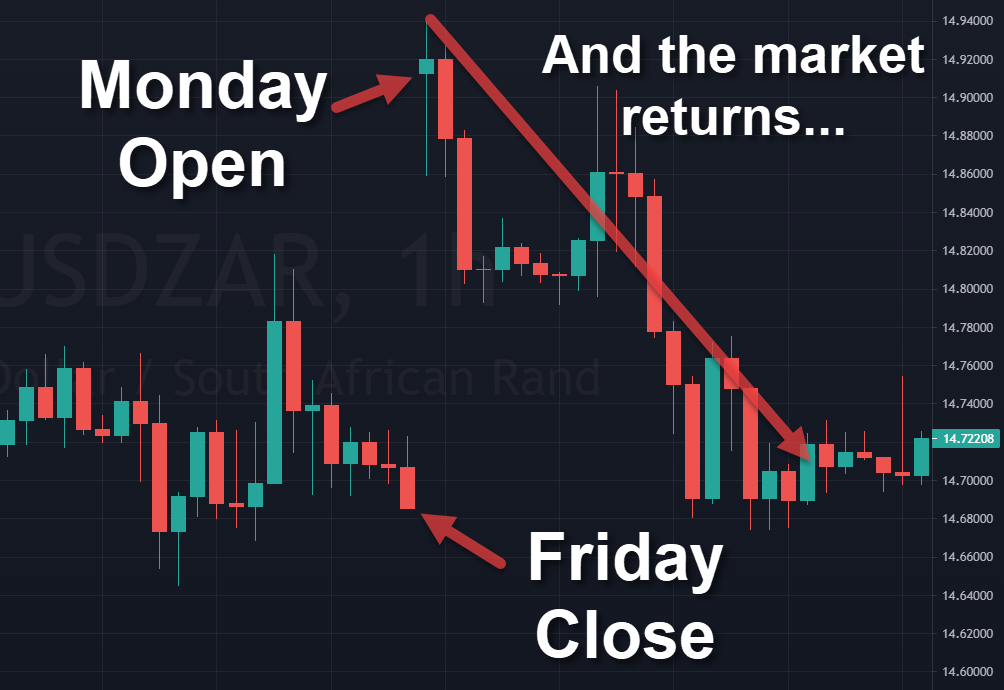

As we mentioned earlier, the week started with a bang – a market ‘gap’ of 23c is not something to be sniffed at.

However, as we often see with one of these moves, when there is that vacuum generated, the market often moves to fill it. Which it did, as shown out perfectly in the chart from Monday:

The USDZAR quickly retreated from it’s highs of R14.94, to break down to R14.67, nearly 30c lower again in just a few hours.

A volatile start…but this is something we have come to expect!

None the less, our forecast remained accurate and in play, and we waited to see what the coming days would bring.

And interesting news certainly did come, as the shipping industry became the focus of world news. Freight has already been disrupted and fairly chaotic for the last 12 months, but things got taken to another level this time with a huge Evergreen cargo ship getting stuck across the Suez Canal.

The result was that ships were blocked entering or exiting this key shipping route, and if anyone doubts how crucial it is, this one simple stat doesn’t lie:

Every day that the ship sits there, it is affecting approximately $9.6 billion a day worth of ship traffic!

This is absolutely staggering, and gives an idea of just how many goods are moving around everywhere, everyday. And that is just one shipping route, albeit a very critical one!

With it possibly taking some weeks to unblock the Evergreen, this could severely impact trade and commodity prices in the coming months.

Locally, the big news was everyone waiting on SARB’s interest rate decision which was on Thursday…

Thursday duly came, and by this stage the Rand was already trading weaker again, up around R14.95.

Reserve Bank announced the expected of the repo rate staying at 3.5%, and the prime rate at 7%. Expectations were also for inflation to remain contained into 2021, and GDP projections were upped slightly to 3.8% for 2021, rather than 3.6%.

All good news, right? Well, the Rand didn’t think so, as it weakened further to break as far as R15.09 to the Dollar, right in line with our forecast expectations – as the Dollar Index pushed to it’s best levels since November last year!

And then in other big news…

- Another big event on Monday was this: Chinese officials were sanctioned by the US and EU in a “coordinated action“ to address human rights violations in Xinjiang. Beijing retaliated furiously, imposing sanctions of their own, with this negative sentiment taking a toll on global equity markets and EM currencies alike (this could be one to keep your eyes on in the coming days…)

- In Europe, a major consideration was how the extensions of lockdown restrictions have weighed on risk appetite, with EM currencies on the back foot as investors move to safer assets. Amidst growing resistance and mass protests across the continent against lockdowns and the ‘gene therapy’ experimental ‘vaccines’, some countries have nevertheless been gearing up for new restrictions in an attempt to combat a feared ‘third wave’. Germany was one of these, but then Angela Merkel reversed her decision for a lockdown over Easter – perhaps some sanity is starting to prevail! As already mentioned, there is no proof that lockdowns & restrictions (or masks) have been needed – or have worked. In fact, they have caused far more damage and ill-health than the virus itself.

- Crude oil has been skyrocketing over the last few months, leaving little respite for fuel prices. But this week the price of brent crude oil has dropped to $60/barrel after peaking at $71/barrel. We can only hope this could provide relief down the line for motorists who will be paying more to fill up their tanks in April.

- And then there was Eskom…with risks of load shedding still very apparent for the coming years, the current problem the Treasury is faced with is the load of debt that the SOE has generated. Now setting at nearly R500bn, a decision must be made whether to move this into a special-purpose vehicle or have the state take over responsibility for it directly. As Fin24 put it, it is now a case of the lesser of the two evils as to how the Treasury can proceed. Some dangerous days ahead as SA’s main source of power remains on the ropes…

And getting back to the Rand, Friday saw the market pull back slightly from Thursday’s push higher, ultimately closing around R15.05 at the end of local trade. A rummy old week, but you would have to say the Dollar was back on top with the ZAR back over R15…

The Week Ahead (29 Mar – 2 Apr 2021)

And as we rush toward April at a terrific pace, here are some of the events to keep an eye on during this week, especially Non-Farm Payrolls (very often a major trigger):

- SA – Balance of Trade

- USA – Biden Speech, Jobless Claims, Non-farm Payrolls

- UK & EU – GDP, Consumer Price Index

So where does that leave us as we head into the second quarter?

Well, the Rand has spent a very choppy 3 months between 14.40 and 15.66 and the longer we stay in this band, the more likely an impulsive move out of it. The next couple of weeks will likely prove pivotal and based on our analysis, we will be watching key levels over the next few days.

Please take our Rand forecasting service for a test-drive!

This will give you access to the same charts we are to give us and our clients the likely direction of the Rand – ahead of time, enabling you to make educated and informed decision. Simply use the link below to get access now. No charge. No card. All yours to trial for 14 days.

Click here to access to our forecast from Friday on the house!

If you have any questions or feedback, please let me know.

To your success~ James Paynter