Preparing for the 2021 SETA submission period, it is important to reflect on the last 12-months and consider the economic impact caused by the Covid-19 global pandemic and how it affected various organizations’ ability to continue to develop their workforce.

With many organisations ceasing to operate during the hard-lockdown levels, learning and development took a backseat as the focus moved away from growing and thriving, to simply surviving. However, certain aspects of learning and development cannot be ignored, specifically regarding training conducted for B-BBEE purposes.

Fortunately for the proactive, there are existing relief measures designed for the purpose of assisting with one’s training budget in the form of various grants and tax rebates.

Mandatory and Discretionary Grants:

Whilst most businesses are aware of their annual reporting requirements with the SETAs, a vast majority are only aware of the “Mandatory Grants” that are available to them.

To simplify, a “Mandatory Grant ” is paid annually to organizations for reporting on their completed training (under the Annual Training Report) and their planned training (under the Workplace Skills Plan). This grant equates to 20% of the Skills Development Levies or SDL which is a monthly 1% levy paid to SARS based on the total salaries and wage bill by organizations with a payroll equal or more than R 500,000 per annum.

“Discretionary Grants” are simpler to understand as these grants are awarded to an organization at the discretion of the SETA. So-called “Discretionary Grant-windows” open sporadically throughout the year, with specific requirements communicated to all interested organizations. These requirements can be for a specific training programme, a specific field or job title, or could simply be available for training programmes that align to the specific SETA’s Sector Skills Plan (SSP) which is a formal document, published annually, indicating the scare and/or critical skills with the hard-to-fill vacancies identified within the industry of the specific SETA. The value of a “Discretionary Grant” can add up to 49.5% of an organization’s annual paid Skills Development Levies.

The Employment Tax Incentive (ETI):

The Employment Tax Incentive (ETI) is an incentive introduced by SARS in 2014 to encourage organizations to hire young and less experienced job seekers. This incentive is applied monthly when submitting the monthly SARS EMP201 Employer Declaration Form to SARS and the process itself, is managed either by the payroll or finance departments. There is no limitation on the number of employees that may be claimed and this incentive is also effective till 2029.

For an organisation to be eligible, they must:

- Be registered for Employee Tax (PAYE), or must be eligible to register for PAYE,

- Not be operating in the national, provincial, or local spheres of government,

- Not be a public entity listed in the Public Finance Management Act,

- Not be a municipal entity, and

- Not be disqualified by the Minister of Finance due to the displacement of an employee or by not meeting the conditions that may be prescribed by the Minister via a regulation.

For an employee to qualify, he or she must:

- Have a valid South African ID, Asylum Seeker permit or an ID issued in terms of the Refugee Act,

- Be between the age of 18 to 29 years old,

- Not be a domestic worker,

- Not be a “connected person” to the employer,

- Be employed by the employer or an associated person to the employer on or after 1 October 2013, and

- Be paid the minimum wage applicable to that employer or if a minimum wage does not apply, is paid the amount contemplated in the Minimum Wage Act and not more than R6 000 remuneration per month. If there is no prescribed wage regulating measure or not subject to or exempt from the requirements of the National Minimum Wage Act, a wage of at least R2 000 (where the qualifying employee was employed for 160 hours in a month) must be paid.

The 12H Learnership Allowance:

The 12H Learnership Allowance was introduced to motivate employers to develop their employees and is made available in two parts i.e. an Annual Allowance and a Completion Allowance. This allowance is seen as a tax credit and is deducted annually at the end of the tax assessment period.

An employer will only qualify for the Annual Allowance if:

- During any year of assessment, the learner is a party to a registered learnership agreement with the employer,

- The learner holds an NQF-level qualification ranging from NQF Level 1 to 10,

- The agreement was entered into pursuant to a trade carried on by that employer, and

- The employer has derived “income”, as defined, from that trade.

An employer will qualify for the Completion Allowance if they meet the criteria for the Annual Allowance above and if the learner(s) have successfully completed the learnership programme during the year of assessment.

An employer will not qualify for any part of this allowance, during any assessment period, in which there is no registered learnership agreement and if the claimed learner is not employed.

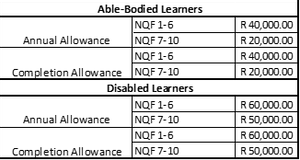

Both allowances can be broken down as per the below table, with a pro-rata amount applicable should the programme not run for the full 12-months of the tax assessment year:

By taking advantage of the above relief measures and shifting one’s thinking around what learning and development is, how it should be implemented and what it entails, it is possible for all organizations to meet their training needs and to continue to upskill their workforce.

For proper compliance with the Skills Development Act and to ensure your organization meets the set B-BBEE targets and/or applicable requirements, it is critical for organizations to have a good working relationship with their preferred training providers. Alternative options and methods should be in place to meet training needs whilst also adhering to all levels of lockdown regulations and different budget-friendly payment solutions should also be made available.

For more information on the above topic, please contact the LabourNet Helpdesk at 0861 LABNET (0861 522638).

Not yet a LabourNet client, but would like to know more about our service and products?

Email us: support@labournet.com / portelizabeth@labournet.com / eastlondon@labournet.com