For many young people the idea of saving for retirement seems like something that needs to be done only when one is much older, more settled, or has paid off debts.

“But then we hear the scary statistic highlighting that only 6% of South Africans can afford to retire financially independent. That is a truly worrying statistic and something that needs to be changed for the better over time,” says Ester Ochse, Product Head: FNB Money Management.

“Financial independence is defined as not needing financial support from family, friends or the government.

“The big question is when should a person start saving and investing for retirement? And the answer is simple, the sooner the better, even contributing a small amount to retirement savings now can be very beneficial in the long run.”

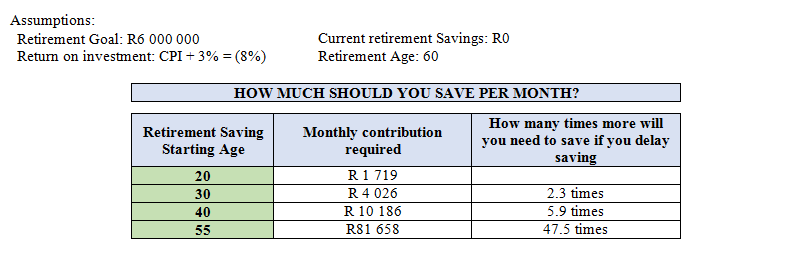

Let’s use an example of why it is better to start earlier to save for retirement, rather than later. This example is of someone targeting a lump sum of R6,000,000 at retirement, which should give them a sustainable income of R25,000 per month (increasing with inflation) until the age of 90.

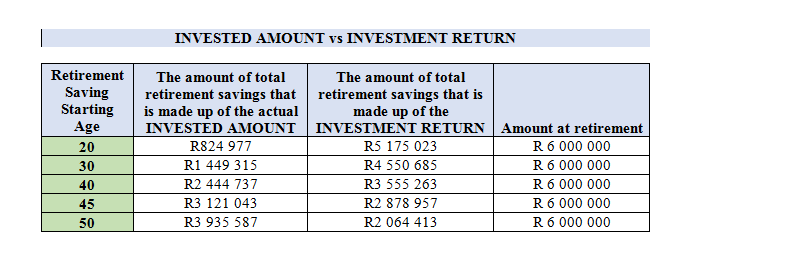

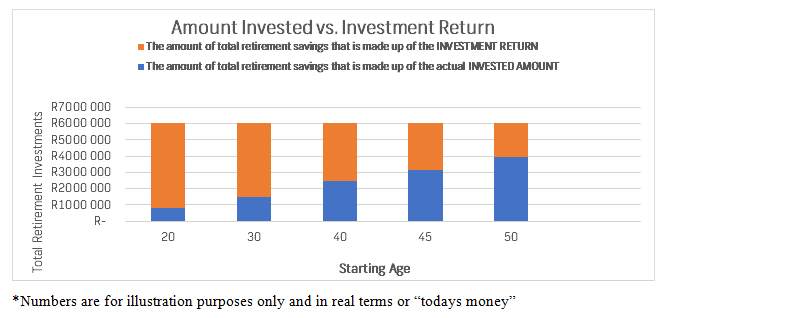

“So, when one looks at the illustration below one can see that to get to the same lump sum at retirement being R6,000,000 until the age of 40 most of the amount is made up of interest and returns in the investment,” adds Ochse.

“At about 45, the returns and contributions start equalling and after that it is the contributions that exceed the returns.”

The moral here is that the earlier a person starts saving for retirement, the more they can benefit on the effects of compound interest. This means that the interest earns interest, over a long period of time.

When it comes to retirement, there are a few things that one needs to consider:

- What are your retirement goals and how much do you need for those goals?

For example, someone that wants to regularly travel in retirement will need more in retirement than someone that wants to be a homebody.

- Continue to budget in retirement

Critically look at your budget now and see how many of those expenses will carry on into retirement. For example, groceries will continue into retirement but traveling to work and back will not.

- Make provision for increased medical cover and expenses in retirement

Getting older generally means more medical expenses, ensure that you work that into the budget. Medical inflation is notoriously higher compared to consumer price inflation; therefore, you need to take this into account.

- Make sure that you invest in the right solution for the right time horizon

Solutions you invest in need to be appropriate for your needs. Some solutions protect you against the risk of outliving your pension and other solutions don’t give you protection against longevity risk but provide you with flexibility on the income that you select annually. Do your research and get advice from appropriately qualified and registered financial service providers.

- Preserve your retirement savings

When you change an employer and have a pension fund from the previous employer, preserve your retirement savings in one of the vehicles that are available like a preservation fund or the new employers pension fund.

The reason why most people do not retire comfortably is because they do not preserve their pension when changing jobs. This will help towards the effect of compound interest and is a good practice in the long run.

“The next step is freeing up cash to contribute towards your retirement goals. Get back to the basics of checking your budget and see where you are spending your money. Using a tool like track my spend on the FNB App will show you where you will be able to redirect some funds to your retirement savings,” explains Ochse.

“Open and maintain your FNB Retirement Annuity on the FNB App in less than three minutes. The contributions into the FNB Retirement Annuity start from as little as R300 per month.

“Then ensure you include the contributions in your monthly budget by using the FNB Smart Budget tool on the FNB App and stick to your monthly money goals and long term retirement goals.”