The Rand has once again wobbled it’s way to the end of the week, but has ended up sitting a lot more comfortably than it did at the beginning.

It was another week of international focus, as electrical energy costs and supply took centre stage.

It was not just China battling, but Europe now joining them similar issues. And both were giving warning signs for all countries.

But Europe’s problem is quite unique, being a country so reliant on imports.

Right now, energy prices are soaring and there is no clear light on the horizon – only an incoming winter which is sure to make things worse. But let’s get into the full Rand Review – and take a look how these kinds of crises are warning signs for SA and the Rand as well…

Key Moments (11-15 October 2021)

Here were the rest of the big talking points from the week:

- Inflation Persists – despite all promises from the Fed & Co. that inflation was a mere passing whim, it’s persistence continues…

- SA’s Coal Power – with it’s own energy problems, SA is watching keenly to see what the rest of the world does amid the growing energy crisis…but is it taking it’s problems seriously?

So, to begin the week, we had the Rand floating around the R14.90 level, still awaiting a clear breakout either side of the R15/$ turning point…

And this week was surely the one where we were going to get some clarity.

Everything was primed for volatility, as we head into the end-of-year period – which just has a reputation for being that way!

And there was the brewing crisis in Europe that we had already touched on.

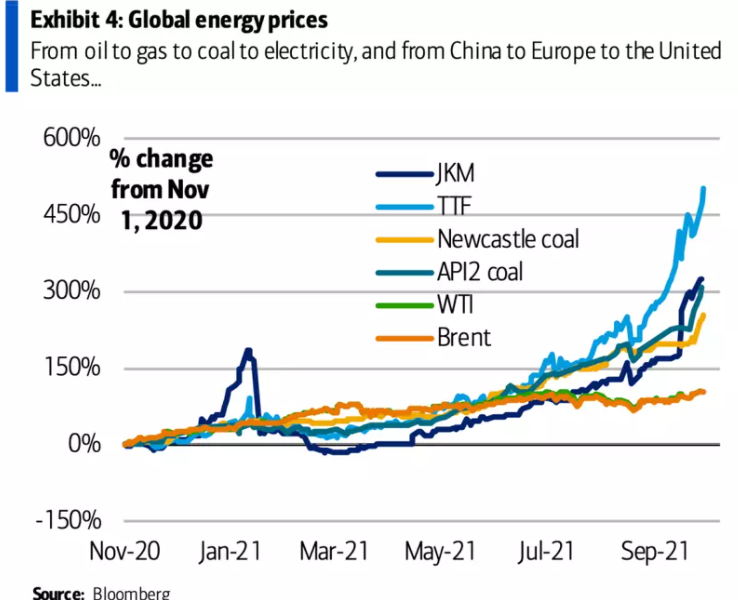

Europe’s position is not a good one, as they are heading into another winter, and energy prices are on a one way track higher at the moment. This is not just a Europe problem, with oil prices, fuel prices etc across the whole word suffering badly – or rather, consumers suffering badly, as a result of this! Here is a chart from Bloomberg showing just how bad it has become:

This is just adding to the host of problems that the UK is facing, with Brexit having already created complications like nothing else for the supply chains in the region.

As we head into a period of the holiday season, there is never a time where supply chains are under more strain – and the perfect storm since the beginning of the ‘pandemic’, to the blocking of the canal and much more!

It never rains, but it pours!

As for the Rand, the first half of the week was shaky on all of this news as markets looked largely very unsettled by this news… …firstly we saw the local unit up to near R15.10, before gaining ground again into the end of the week, and back to sub-R14.75 heading into Friday!

And then in other news:

- Inflation is something that the US Fed has tried to play down over the course of the last 10 months or so, but as 2021 has gone on, it has become near impossible to deny. Now it looks like it is going to finally result in there being some action taking, with talk of tapering of their spending programs toward the end of this year. Commodities are up, shipping and freight is up, cost of fuel is up, everything is more expensive…so what comes next, as we head into the last few weeks of this year? We are in for some really interesting economic days in the close of 2021.

- And getting back to energy again, SA is watching with anticipation at the coal situation in China – as well as trying to fight Eskom’s own fires of an unstable power grid. SA is in very similar position where most power comes from coal, and is being forced between a rock and a hard place to move toward more renewable energy – but not having the funding or grid stability to make it happen. Yet despite that, Mantashe, SA’s energy minister, is inexplicably taking a bullish stance that rich nations must not bully South Africa – and force SA to ban new coal-power projects. However, this seems to be a fairly short-sighted approach, as SA’s need for funding means that there is hardly room to make your own rules or terms…!

- Lastly, in line with all the other points we have discussed was the economic data and reports from the week. Uninspiring US employment data released yesterday have sparked early fears that stagflation is on the horizon. This could result in the Fed beginning its asset-tapering program sooner than expected, leaving the rand, and other emerging market currencies, in a vulnerable position. The Fed then once again indicated that they could start the tapering process as early as mid-November with a target date to end purchases in mid-2022. Fed officials remain concerned about persistent inflation as confirmed by yesterday’s CPI data (5.4% vs 5.3% expected). The data remains “hot” considering the Fed’s target inflation rate is 2%. Locally, there was some better news with SA’s growth forecast being adjusted to 5%, even as the global growth outlook was being pushed downwards.

As for the Rand, we saw more of the same on Friday, as the Rand pushed steadily stronger to begin testing the R14.60, R16.90 and R20.00 levels to the Dollar, Euro and Pound respectively.

So while on shaky ground, the Rand rounded off the week in very solid fashion – which meant it got to start a new week on the front foot!

The Week Ahead (18-22 October 2021)

And so as we head further into the week, we have very limited fundamental data that could provide some triggers:

- SA – Inflation Rate

- US – Jobless Claims

- UK – Inflation Rate

But nevertheless, the markets remain jittery from an economic, financial, political and social perspective, which means volatility is not likely to taper off.

Once again, we will try and cut through all the noise by focusing on what the market patterns themselves are telling us (based on our Elliott-wave based forecasting system), giving us and our clients an objective view on where the market is expected to head in the days, weeks and months ahead.

Please take our Rand forecasting service for a test-drive! This will give you access to the same charts we are to give us and our clients the likely direction of the Rand – ahead of time, enabling you to make educated and informed decision. Simply use the link below to get access now. No charge. No card. All yours to trial for 14 days.

Click here to access to our forecast from Friday on the house!

If you have any questions or feedback, please let me know.

To your success~ James Paynter